By Scott Neill | Published: May 5, 2026 | Last Updated: June 2026

A North Texas driver is heading home on a normal afternoon. Traffic slows, they look down for a second, and rear-end the vehicle in front of them.

Within weeks, medical bills, lost wages, and vehicle damage start adding up.

Total claim value, $450,000.

The at-fault driver has Texas minimum coverage.

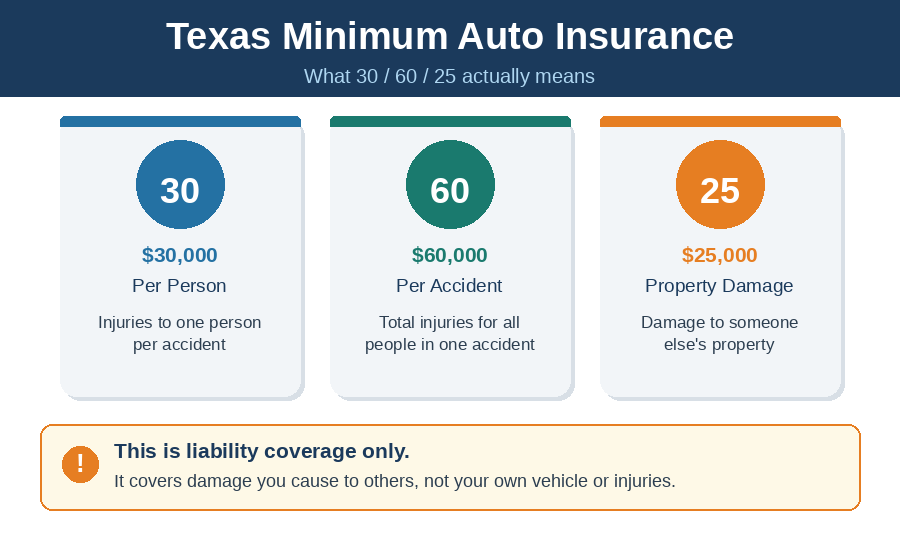

They are covered for $30,000 per person, $60,000 per accident for injuries, and $25,000 for property damage.

Everything above that limit becomes their responsibility. At Neill Insurance Brokers, we see this exact scenario happen all too often—and that is where the real problem starts.

Everything above that limit becomes their responsibility. At Neill Insurance Brokers, we see this exact scenario happen all too often—and that is where the real problem starts.

Our founder Scott Neill spent 10 years working as a captive Farmers agent before launching Neill Insurance Brokers as an independent agency. Having reviewed thousands of North Texas auto policies, and with our team now managing 304 active homeowner accounts and over $6 million in total premium, we know firsthand that Texas state minimums are mathematically out of date. We’ve watched real families face lawsuits and asset garnishment simply because their policy limits ran out in less than a second after a crash.

What Texas Minimum Auto Insurance Actually Covers

Why Minimum Coverage Falls Short in Real Accidents

Medical Costs Add Up Quickly

An ambulance ride can cost thousands.

Emergency care, imaging, and follow-up treatment can easily exceed $30,000 for one person.

Multiple Injuries Create a Bigger Problem

If three people are injured, your total coverage is capped at $60,000.

That means the insurance company divides that amount among all injured parties.

Vehicle Costs Are Higher Than Ever

The average cost of a newer vehicle continues to rise.

A single totaled SUV or truck can exceed $40,000.

Your policy only covers $25,000 for property damage.

What Happens When Your Coverage Is Not Enough

When your liability limits are exceeded:

- Your insurance pays up to your limit

- You are personally responsible for the remaining balance

- You can be sued for the difference

In Texas, courts can pursue:

- Bank accounts

- Future income

- Certain personal assets

What Better Coverage Looks Like

For most North Texas drivers, a safer starting point is:

- $100,000 per person

- $300,000 per accident

- $100,000 property damage

This is often referred to as 100, 300, 100 coverage.

It provides significantly more protection in a serious accident.

The Role of an Umbrella Policy

Even higher limits may not be enough in a major accident.

That is where an umbrella policy comes in.

An umbrella policy adds an extra layer of liability protection above your auto and home policies.

For many families, $1 million in umbrella coverage costs around $400 to $600 per year.

It is one of the most cost-effective ways to protect your assets.

Frequently Asked Questions

What are the legal minimum auto insurance limits required in Texas?

Texas law requires a minimum 30/60/25 liability coverage. This legally mandates up to $30,000 for bodily injury per person, a total of $60,000 for bodily injury per accident (regardless of how many people are hurt), and $25,000 for property damage liability.

Why is Texas state minimum liability insurance not enough?

It falls short because real-world accident costs easily exceed these outdated 20-year-old limits. The average cost of a new vehicle in Texas is over $40,000, meaning a $25,000 property damage limit won’t even cover a totaled standard SUV. Furthermore, a single overnight hospital stay or ambulance ride can instantly blow past the $30,000 medical limit.

What happens if I cause an accident and my insurance limits are exceeded in Texas?

Once your insurance company pays out up to your policy limit, your legal defense stops and you become personally liable for the remaining balance. The injured party can sue you directly, and Texas courts can issue judgments to target your non-exempt savings, liquid bank accounts, and future disposable income.

What auto insurance liability limits do independent brokers recommend?

For adequate protection, most independent insurance brokers recommend carrying at least 100/300/100 liability limits ($100,000 per person, $300,000 per accident, and $100,000 for property damage). If you own a home or have significant financial assets, it is highly recommended to stack a $1 million personal umbrella policy on top of those limits.

What This Means for You

Minimum auto insurance in Texas meets legal requirements. It does not guarantee financial protection.

The gap between minimum coverage and real-world accident costs is where most people are exposed.

This is not about selling more insurance. It is about understanding the risk before something happens.

The good news is that fixing this gap is simple. A short review of your policy can show you exactly where you stand and what adjustments make sense for your situation.

If you have not looked at your liability limits recently, now is the time.