By Scott Neill | Published: April 3, 2026 | Last Updated: July 2026

Quick Summary

This article, with insights from Neill Insurance Brokers, explains how wind and hail deductibles work in Texas homeowners insurance, highlighting why many homeowners face unexpectedly high out-of-pocket costs after storms. It details the common practice of setting deductibles as a percentage of the home’s value, the financial trade-offs involved, and how to structure your policy to avoid costly surprises during claims.

Key Takeaways:

- Wind and hail deductibles in Texas are often set as a percentage of your home’s insured value, which can result in thousands of dollars owed before insurance pays.

- Increasing your deductible from 1% to 2% can lower your annual premium by $150 to $400 but may double your out-of-pocket costs during a claim.

- Many homeowners mistakenly assume their deductible is a flat dollar amount like auto insurance, overlooking the significant financial risk tied to percentage-based deductibles.

- Texas homeowners typically have two deductibles: one specifically for wind and hail damage and another for all other types of claims, which affects how and when you pay out-of-pocket.

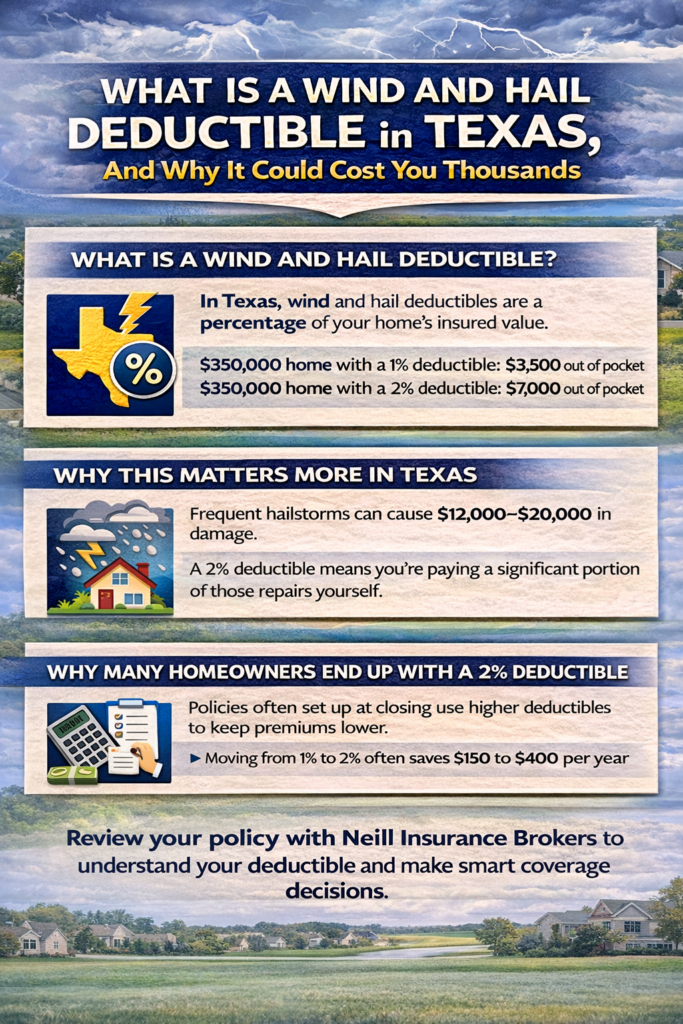

Having spent 10 years as a captive Farmers agent before founding Neill Insurance Brokers, Scott Neill has seen firsthand how severe seasonal weather impacts local homeowners. In 2026, Texas insurers rely heavily on percentage-based deductibles to offset the state’s extreme storm risks. Unlike flat fees, this amount is calculated as a fixed percentage (1%–3%) of your total dwelling coverage. For a $400,000 home with a 2% deductible, you’ll pay $8,000 out-of-pocket before hailstorm repairs are covered.

Why This Matters More in Texas Than Anywhere Else

Texas, especially North Texas, sees frequent and severe hailstorms.

In areas like Roanoke and Keller, major hail events cause widespread damage every year. A single storm can impact thousands of homes at once.

Here is a real example most homeowners do not think about:

A roof replacement in the Dallas Fort Worth area typically costs between $12,000 and $20,000.

If your deductible is $7,000, you are paying a significant portion of that cost yourself before insurance contributes anything.

Why Most Homeowners End Up With a 2 Percent Deductible

Your policy was likely set up during your home purchase, not during a thoughtful insurance review.

At closing, the goal is to get a policy in place quickly and keep your monthly payment within budget.

The easiest way to lower your premium is to increase your deductible.

- Moving from 1 percent to 2 percent may save $150 to $400 per year

That small savings often goes unnoticed. What does not get explained is the trade off.

That same decision can increase your out of pocket cost by thousands during a claim.

The Trade Off Most Homeowners Do Not Realize

Many people believe choosing a higher deductible is always the smarter financial move.

That assumption breaks down when the deductible exceeds what you can comfortably afford.

For example:

Saving $300 per year over five years equals $1,500 in savings.

But increasing your deductible from $3,500 to $7,000 adds $3,500 in risk.

You are taking on more than double the potential cost for a relatively small annual savings.

Insurance is designed to transfer risk, not shift it back onto you.

You Actually Have Two Deductibles

Most Texas homeowners do not realize this.

Your policy includes both a wind and hail deductible and an all other perils deductible.

Wind and Hail Deductible

Applies to storms, hail, wind, and hurricanes. Usually percentage based.

All Other Perils Deductible

Applies to fire, theft, burst pipes, and other non weather events. Often a flat dollar amount, but not always.

Here is where problems happen:

Some policies use percentage deductibles for both.

That means a water damage claim could carry the same $7,000 deductible as a hail claim.

A properly structured policy separates these to reduce your financial exposure.

What a Well Structured Policy Looks Like

A strong homeowners policy in North Texas typically includes:

- Wind and hail deductible, 1 percent of dwelling coverage

- All other perils deductible, $1,500 to $2,500 flat

- Updated dwelling coverage based on current rebuild costs

- Key endorsements like water backup and service line coverage

This structure balances premium savings with real protection when you need it most.

Across our Texas clients, many homeowners fall into the $2,500 to $3,500 annual premium range depending on home value and location.

How to Find Your Deductible Right Now

You can check this in a few minutes.

- Open your homeowners policy or declarations page

- Find the section labeled deductibles

- Look for wind and hail and all other perils

If you see a percentage, multiply it by your dwelling coverage.

That number is what you will pay out of pocket before insurance contributes.

Frequently Asked Questions

What is a typical wind and hail deductible in Texas?

Most policies use a 1 percent or 2 percent deductible based on your home’s insured value.

Is a 2 percent deductible too high?

It depends on your financial situation. If you can comfortably afford the out of pocket cost, it may work. If not, it creates significant risk.

Why are deductibles percentage based in Texas?

Insurance companies use percentage deductibles to manage the high frequency of storm related claims in the state.

Can I change my deductible?

Yes, in most cases you can adjust your deductible at renewal or during a policy update.

How do I find my wind and hail deductible?

You can locate your deductible percentages and flat amounts directly on the declarations page of your homeowners insurance policy.

Know Your Number Before the Storm Hits

If you have ever assumed your homeowners insurance would fully cover you after a storm, you are not alone. Many Texas homeowners only discover their true out of pocket cost after a claim happens.

The next step is simple and important. Know your number before you need it.

At Neill Insurance Brokers, we help homeowners review their policies, understand their deductibles, and make sure their coverage fits their financial reality.

If you want confidence in your coverage, schedule a free policy review and see exactly where you stand.