By Scott Neill | Published: May 15, 2026 | Last Updated: June 2026

Water damage is one of the most common and expensive homeowners insurance claims in Texas. But it is also one of the most misunderstood.

Many Texas homeowners assume that if water damages their home, their insurance policy will automatically cover it. Unfortunately, that is not always true. The source of the water, how quickly the damage occurred, and whether flooding was involved can dramatically impact what your insurance company will and will not pay for.

In this guide, you will learn what types of water damage are typically covered, what exclusions homeowners should watch for, and when you may need additional coverage like flood insurance or sewer backup protection.

What Water Damage Is Typically Covered by Texas Homeowners Insurance?

Burst Pipes

If a pipe suddenly bursts and damages your walls, floors, or belongings, your policy will typically help cover:

- Water extraction

- Drywall repairs

- Flooring replacement

- Personal property damage

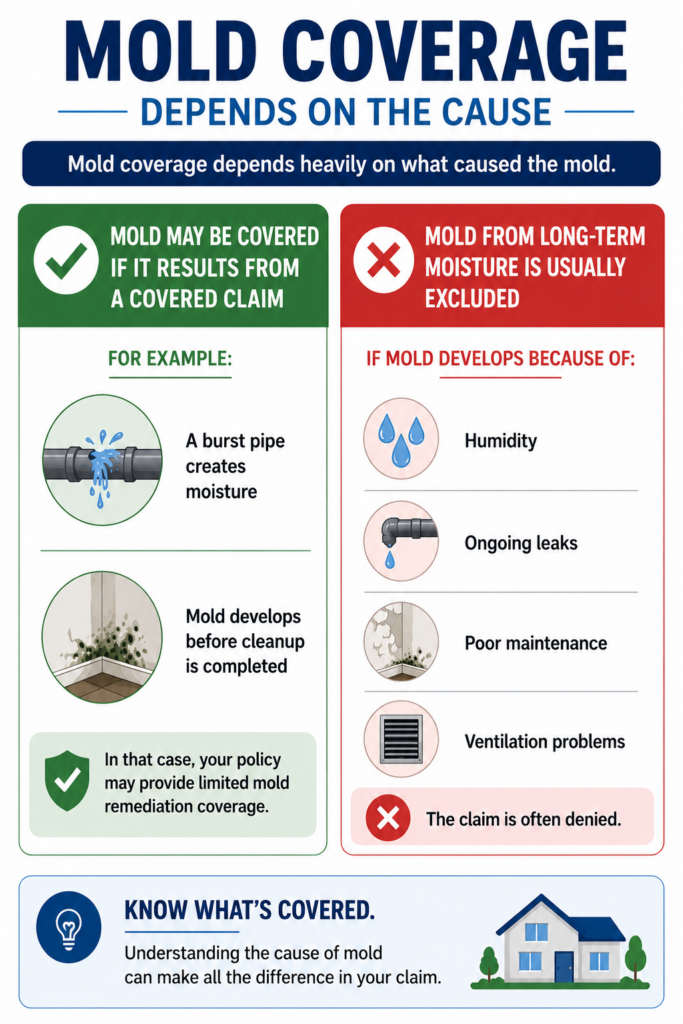

- Mold remediation, in some cases

Accidental Appliance Overflows

Water damage caused by sudden appliance failures is often covered.

Examples include:

- Washing machine hose bursts

- Dishwasher leaks

- Refrigerator line failures

- Water heater ruptures

Sudden Roof Leaks From Storm Damage

If a Texas windstorm damages your roof and rain enters immediately afterward, your homeowners insurance may cover the interior water damage.

Coverage may apply to:

- Ceiling damage

- Wet insulation

- Damaged flooring

- Furniture and electronics

The key factor is that the damage must result from a covered peril, such as hail or wind.

Water Damage From Fire Suppression

If firefighters use water to extinguish a house fire, the resulting water damage is generally covered under your homeowners policy.

What Water Damage Is Usually NOT Covered?

Flood Damage

Flooding is one of the largest exclusions in homeowners insurance.

Flood damage generally includes rising water from:

- Heavy rainfall

- Overflowing rivers

- Storm surge

- Flash flooding

- Surface water runoff

If water touches the ground before entering your home, insurance companies often classify it as flood damage.

Flood damage requires a separate flood insurance policy.

Long-Term Leaks and Neglect

Insurance is designed for sudden accidents, not ongoing maintenance problems.

Claims are often denied for:

- Slow pipe leaks

- Long-term roof leaks

- Rot and deterioration

- Mold from unresolved moisture issues

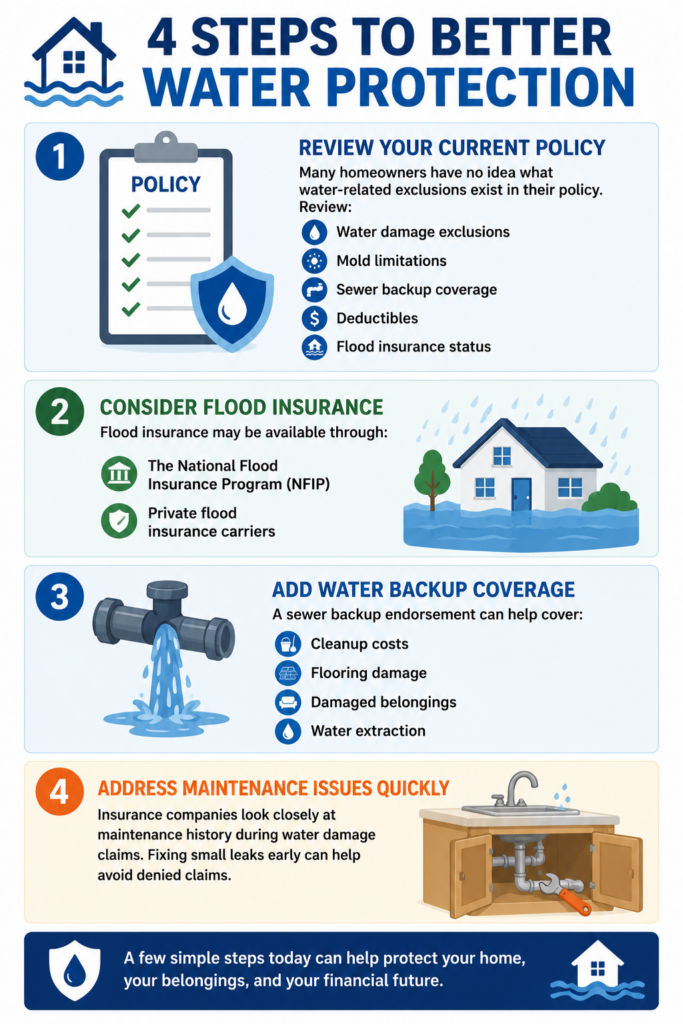

Sewer Backup Without Additional Coverage

Many homeowners are surprised to learn that sewer and drain backups are not automatically included in standard policies.

In his 10 years working as a captive Farmers agent before launching Neill Insurance Brokers, Scott Neill witnessed dozens of families face thousands of dollars in uncovered damages because of this exact missing line. Now managing 304 active homeowner policies and over $6 million in premium across North Texas, our team always double-checks for a specific Water Backup Endorsement to ensure toilet overflows or sump pump failures don’t ruin a family’s budget.

Without a water backup endorsement, damage from backed-up drains or sewer systems may not be covered.

This can include:

- Overflowing toilets

- Sewer line backups

- Sump pump failures

Groundwater Seepage

Water entering through the foundation, slab, or basement walls is typically excluded.

This includes:

- Foundation seepage

- Hydrostatic pressure

- Underground water intrusion

These problems are usually considered maintenance or drainage issues instead of sudden insurance events.

Does Texas Homeowners Insurance Cover Mold?

Why Flood Insurance Matters in Texas

Texas experiences some of the highest flood losses in the country.

Yet many homeowners still assume flood insurance is only necessary near the coast.

The reality is that inland flooding happens frequently across Texas due to:

- Flash flooding

- Severe thunderstorms

- Tropical systems

- Poor drainage

- Urban runoff

According to FEMA, a large percentage of flood claims occur outside high-risk flood zones.

Homeowners insurance and flood insurance are two completely separate policies.

Without flood insurance, flood damage is generally uninsured.

Common Water Damage Misconceptions

“If Water Damages My Home, Insurance Covers It”

Not always.

Coverage depends on the source of the water and whether the event qualifies as sudden and accidental.

“Flood Insurance Is Only for Coastal Homes”

False.

Some of the worst flooding in Texas occurs far inland.

“My Insurance Covers Sewer Backup Automatically”

Usually not.

Most policies require an additional endorsement.

Frequently Asked Questions

Is flood damage covered by standard Texas homeowners insurance?

No. Standard homeowners insurance policies in Texas strictly exclude any damage caused by rising surface water or flooding. To protect your home from heavy rainfall, flash floods, or overflowing bodies of water, you must purchase a separate flood insurance policy through FEMA or a private carrier.

Does homeowners insurance cover roof leaks that damage the interior?

It depends on the root cause. If a sudden Texas windstorm or hail punches a hole in your roof and rain pours in, the interior water damage is typically covered. However, if the water leak is caused by an old, worn-out roof, or years of neglected maintenance, the insurance company will likely deny the claim.

What is a water backup coverage endorsement?

Water backup coverage is an optional, high-value add-on endorsement that helps pay for repairs if dirty water backs up through your home’s sewer lines, drains, or sump pump systems. Since standard homeowners policies exclude drain overflows, adding this endorsement is critical for full protection.

Does homeowners insurance cover mold remediation?

Sometimes. Mold may be covered if it results from a covered water loss, but long-term moisture or neglect-related mold is usually excluded.

Looking Ahead

Water damage claims can become incredibly expensive, especially when homeowners discover too late that their policy excludes the type of damage they experienced.

At Neill Insurance Brokers, we help Texas homeowners review their current coverage, identify protection gaps, and compare options for homeowners insurance, flood insurance, and water backup coverage. Your next step should be reviewing your current policy before the next storm or plumbing issue turns into a major financial problem.

Because when it comes to water damage, knowing what is covered before a loss happens can make all the difference.