By Scott Neill | Published: May 21, 2026 | Last Updated: June 2026

A hail storm hits your North Texas neighborhood.

Your roof is damaged badly enough that it needs to be replaced. The contractor estimates the replacement cost at $16,000. You file a homeowners insurance claim expecting your policy to help cover the loss.

Then the insurance check arrives. It is for $7,200. The remaining $8,800 comes out of your pocket.

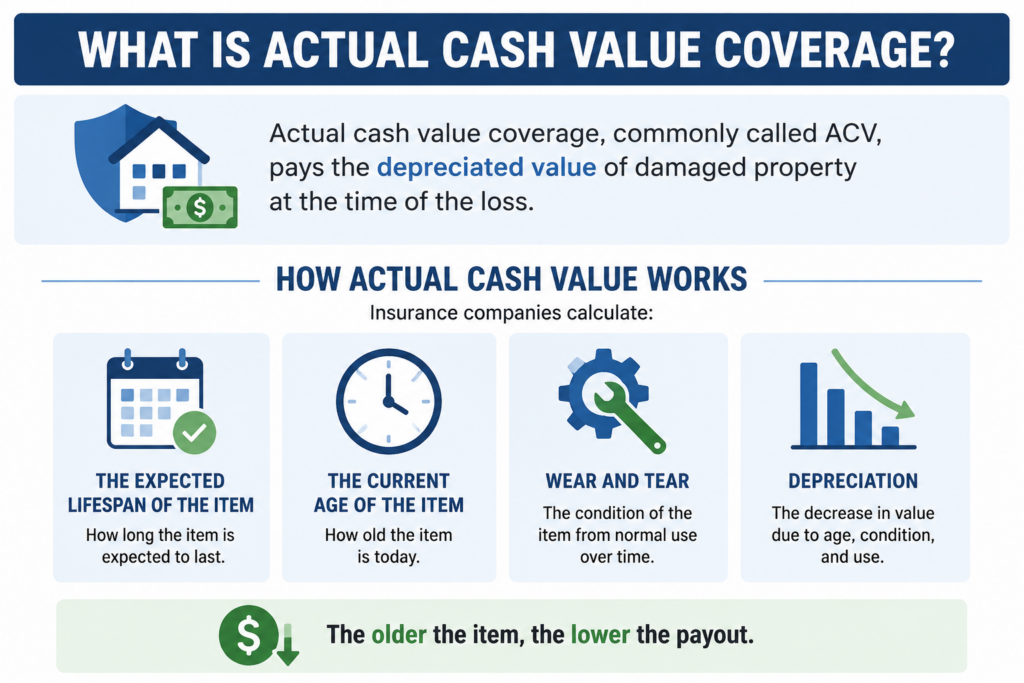

This happens to Texas homeowners every year, especially in hail-prone areas across North Texas. Most homeowners never realize they have actual cash value coverage until after they file a claim.

At Neill Insurance Brokers, one of the biggest coverage gaps we uncover during policy reviews involves replacement cost versus actual cash value coverage. In this article, you will learn the difference between the two, how depreciation impacts claims, where these coverages apply, and how to determine what type of policy you currently have.

What Is Replacement Cost Coverage?

Replacement cost coverage, often called RCV, pays what it costs to repair or replace damaged property with a new equivalent item.

What Replacement Cost Means

With replacement cost coverage:

- Depreciation is not deducted

- The goal is restoring the damaged property with comparable new materials

- Claims generally provide significantly larger payouts

For example:

- Your roof replacement costs $16,000

- Your deductible is $2,000

- Your insurance settlement may pay approximately $14,000

The age of the roof matters much less under replacement cost coverage.

Why Homeowners Prefer Replacement Cost

Most homeowners choose replacement cost because it provides more predictable protection after a major loss. This is especially important in Texas, where hail storms regularly create expensive roof claims.

Example of ACV on a Texas Roof

Let’s say:

- Your roof replacement costs $16,000

- The roof is 15 years old

- The carrier assumes a 20-year roof lifespan

The insurance company may depreciate a substantial portion of the roof value before issuing payment. That could leave you responsible for thousands of dollars beyond your deductible.

With ACV coverage, homeowners are effectively self-insuring part of the replacement cost.

What Many Homeowners Miss

Many homeowners assume: “My home is insured for replacement cost.” But that may only apply to certain portions of the policy.

During his 10 years as a captive Farmers agent and after reviewing hundreds of North Texas homeowners policies, our founder Scott Neill found that this is the exact loophole that catches families off guard. Today, managing 304 active homeowner policies and over $6 million in premium at Neill Insurance Brokers, our team consistently uncovers hidden exclusions where carriers sneak in an ACV endorsement specifically for the roof surface while leaving the main dwelling on RCV.

Some carriers now write:

“My home is insured for replacement cost.”

But that may only apply to certain portions of the policy.

Some carriers now write:

- Replacement cost on the dwelling

- Actual cash value specifically on the roof

That distinction can create major surprises during claims.

How Depreciation Impacts Roof Claims

Most Texas insurance carriers assume asphalt shingle roofs have an expected lifespan of approximately 20 to 25 years.

The Older the Roof, the Larger the Gap

For example:

| Roof Age | Likely Depreciation Impact |

|---|---|

| 3 years old | Minimal depreciation |

| 10 years old | Moderate depreciation |

| 15 years old | Significant depreciation |

| 20 years old | Very limited claim payout |

A homeowner with an older roof may receive dramatically less under ACV coverage than under replacement cost coverage.

The Premium Difference Is Often Smaller Than Expected

The annual premium difference between ACV and replacement cost roof coverage is commonly around:

- $150 to $300 annually

One hail claim can easily outweigh years of premium savings.

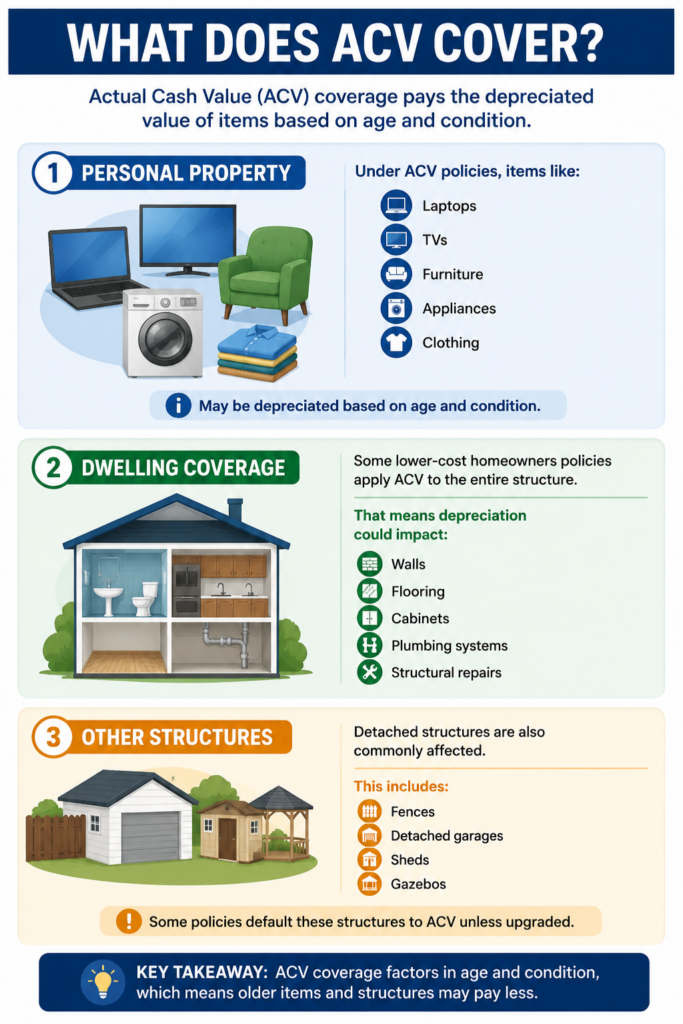

ACV vs. Replacement Cost Applies to More Than Roofs

How to Find Out What Coverage You Have

The easiest place to start is your homeowners insurance declarations page.

Look for These Terms

Replacement Cost Coverage

You may see:

- Replacement Cost

- RCV

- Replacement Cost Loss Settlement

This generally indicates stronger coverage.

Actual Cash Value Coverage

You may see:

- Actual Cash Value

- ACV

- Roof Surface Payment Schedule

This means depreciation applies.

Limited Replacement Cost

Some policies include hybrid language where:

- Depreciation is applied initially

- Additional reimbursement occurs after repairs are completed

This is often called recoverable depreciation.

Pay Close Attention to Roof Endorsements

Even if your dwelling has replacement cost coverage, your roof may still have a separate ACV endorsement.

Look specifically for:

- Roof Loss Settlement

- Roof Surface Payment Schedule

- Cosmetic damage exclusions

When Does ACV Coverage Make Sense?

Older Roofs Near Replacement Age

If your roof is already 18 to 20 years old and nearing the end of its lifespan, the lower premium may outweigh the benefit of replacement cost coverage.

Especially if:

- You already plan to replace the roof soon

- You are budgeting for replacement independently

- You prioritize lower annual premiums

Frequently Asked Questions

What is the difference between replacement cost and actual cash value?

Replacement cost (RCV) pays the full cost to repair or replace your damaged property with brand-new equivalent materials today, without deducting anything for wear and tear. Actual cash value (ACV) deducts depreciation based on the item’s age and condition before issuing your claim check, leaving you to pay the difference out of pocket.

Does Texas homeowners insurance always cover roofs at replacement cost?

No. Due to severe hail storms across North Texas, many insurance companies now automatically attach an “Actual Cash Value” or “Roof Surface Payment Schedule” endorsement to standard policies. This means even if your house structure is covered at replacement cost, your roof claim will still be heavily depreciated based on its age.

Why is ACV coverage cheaper?

No. Many Texas insurance carriers now apply actual cash value endorsements specifically to roofs, even if the rest of the dwelling has replacement cost coverage.

How can I tell if my roof has ACV coverage?

Check your declarations page or endorsements for terms like “Actual Cash Value,” “Roof Surface Payment Schedule,” or “Roof Loss Settlement.”

Is replacement cost coverage worth the extra premium for a Texas home?

For the vast majority of Texas homeowners, yes. The annual premium difference to upgrade from ACV to RCV roof coverage is usually only around $150 to $300. Spending that small amount saves you from getting stuck with an unexpected $8,000+ bill after a single major hail storm.

Moving Forward

Understanding how depreciation works, especially on roofs in hail-prone North Texas, can dramatically impact your financial recovery after a loss.

At Neill Insurance Brokers, we help homeowners review their policies, understand coverage trade-offs, and compare options that align with their budget and risk tolerance. Your next step should be reviewing your declarations page to determine whether your roof and personal property are covered under replacement cost or actual cash value coverage.

Because when a hail storm hits, the difference between RCV and ACV can easily become a difference of thousands of dollars.