Buying a home is exciting. It is also one of the busiest financial transitions most people will ever experience.

Between moving boxes, utility transfers, and closing paperwork, insurance details can easily get overlooked. Unfortunately, missing a key coverage review during your first month of ownership can leave you exposed to unexpected costs later.

If you recently purchased a home in Texas, this checklist will help you make sure your insurance setup is complete during your first 30 days.

4 Key Takeaways

- Review your homeowners policy immediately after closing.

- Verify deductibles, coverage limits, and endorsements.

- Consider flood, umbrella, and other supplemental coverage options.

- Schedule an annual insurance review to keep coverage current.

1. Review Your Homeowners Insurance Policy

Start by reading your declarations page.

Pay special attention to:

- Dwelling coverage limits

- Wind and hail deductibles

- All other peril deductibles

- Personal property coverage

- Liability limits

- Loss settlement method

Make sure the policy accurately reflects your home’s value and your coverage expectations.

2. Confirm Your Rebuild Cost

Many homeowners focus on market value when evaluating insurance.

Insurance companies focus on rebuilding costs.

Construction costs in Texas continue to fluctuate due to labor and material expenses. Review your dwelling coverage to make sure it reflects current replacement costs, not simply what you paid for the home.

3. Understand Your Deductibles

Deductibles can significantly impact your out-of-pocket expenses after a claim.

For example, a 2% wind and hail deductible on a $500,000 home means you could pay $10,000 before insurance contributes to a covered hail claim.

Know your deductible amounts before storm season arrives.

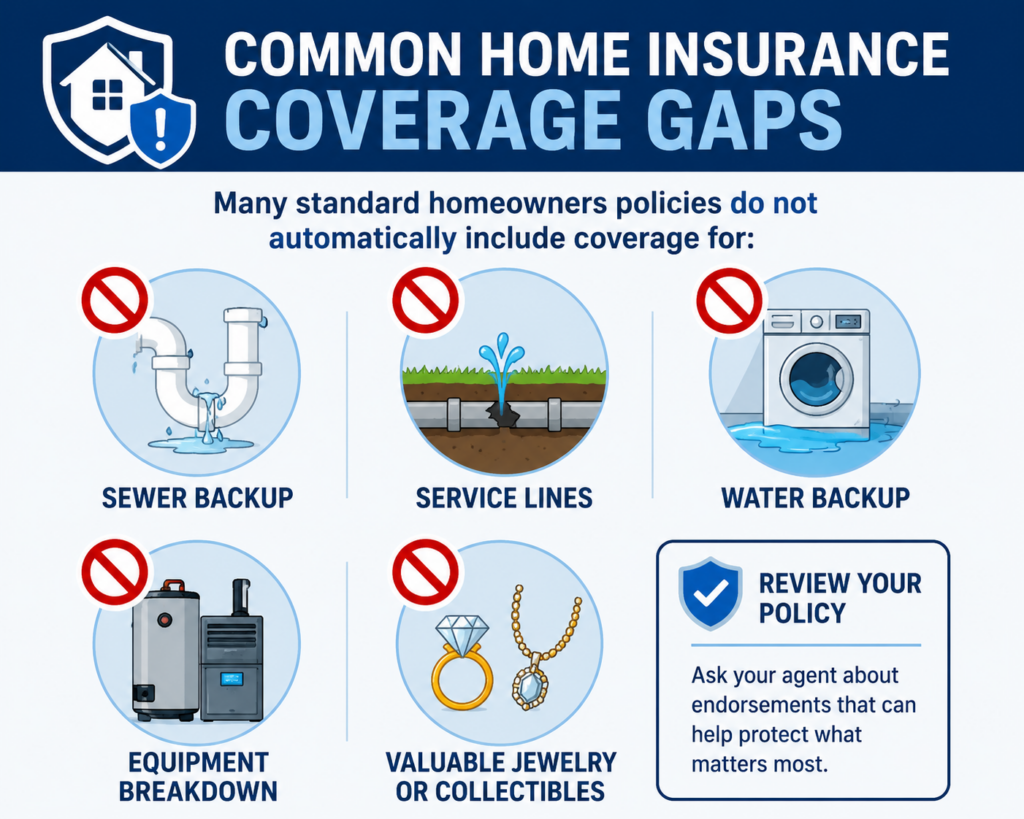

4. Ask About Common Coverage Gaps

5. Determine Whether You Need Flood Insurance

Many Texas homeowners are surprised to learn that standard homeowners insurance does not cover flood damage.

Flooding can occur outside FEMA-designated high-risk zones, and a separate flood insurance policy is typically required for protection.

6. Consider a Personal Umbrella Policy

If you own a home, have savings, host guests, or own recreational vehicles, an umbrella policy may provide additional liability protection above your homeowners and auto insurance limits.

Many umbrella policies provide $1 million or more in additional liability coverage for a relatively modest annual premium.

7. Review Your Auto Insurance at the Same Time

Many homeowners miss opportunities to save money by keeping home and auto insurance with separate carriers.

Bundling may provide:

- Multi-policy discounts

- Simplified billing

- Coordinated coverage

- Easier policy management

8. Create a Home Inventory

Document your belongings before you ever need to file a claim.

Take photos or videos of:

- Furniture

- Electronics

- Appliances

- Jewelry

- Tools

- Collectibles

Store records digitally so they are accessible if a loss occurs.

9. Schedule an Annual Insurance Review

Your insurance needs will change over time.

Home improvements, inflation, vehicle purchases, and life changes can all impact your coverage needs.

A yearly review helps ensure your policies remain aligned with your financial situation.

Frequently Asked Questions

When should I review my homeowners insurance after buying a home?

Ideally within the first 30 days after closing.

Does homeowners insurance cover flood damage?

No. Flood damage generally requires a separate flood insurance policy.

What is the most important part of my homeowners policy?

Coverage limits and deductibles are two of the most important factors because they directly affect claim payments and out-of-pocket costs.

Do I need an umbrella policy?

It depends on your assets, liability exposure, and overall risk profile. Many homeowners find umbrella coverage to be a cost-effective way to increase liability protection.

Your Next Step as a New Texas Homeowner

Buying a home is a major investment, and your insurance program should be designed to protect it properly.

By reviewing your homeowners policy, understanding your deductibles, evaluating flood and umbrella coverage, and addressing common coverage gaps, you can start homeownership with greater confidence.

At Neill Insurance Brokers, we help Texas homeowners understand exactly what their policies cover, identify potential gaps, and make informed decisions about protecting their homes, vehicles, and financial future. A quick insurance review during your first 30 days of ownership can help prevent costly surprises later.