By Scott Neill | Published: June 1, 2026 | Last Updated: June 2026

Most homeowners do not realize how much money they may be leaving on the table by keeping their home and auto insurance with separate companies.

That was the case for one Roanoke family.

They were not unhappy with their insurance. Their homeowners policy had been with one carrier for years, and their auto insurance had stayed with another company since college. But after years of separate renewals and steady premium increases, they finally looked at the total cost.

Combined, they were paying $5,990 per year across both policies.

They wanted to know if that number actually made sense.

At Neill Insurance Brokers, we reviewed both policies together, which is something many homeowners never have done. What we found was not terrible coverage, but an insurance setup that had never truly been optimized.

What the Insurance Review Found

Having spent 10 years working as a captive Farmers agent before launching Neill Insurance Brokers, our founder Scott Neill spent a decade seeing exactly how separate policies drain a family’s budget. Today, our independent agency manages 304 active homeowner policies and over $6 million in premium across North Texas, which allows us to quickly spot these unoptimized setups.

When we ran the numbers for this Roanoke family, the homeowners policy was through Allstate with:

- A $3,780 annual premium

- A 2% wind and hail deductible

- No sewer backup coverage

- Dwelling coverage that had not been updated since 2022

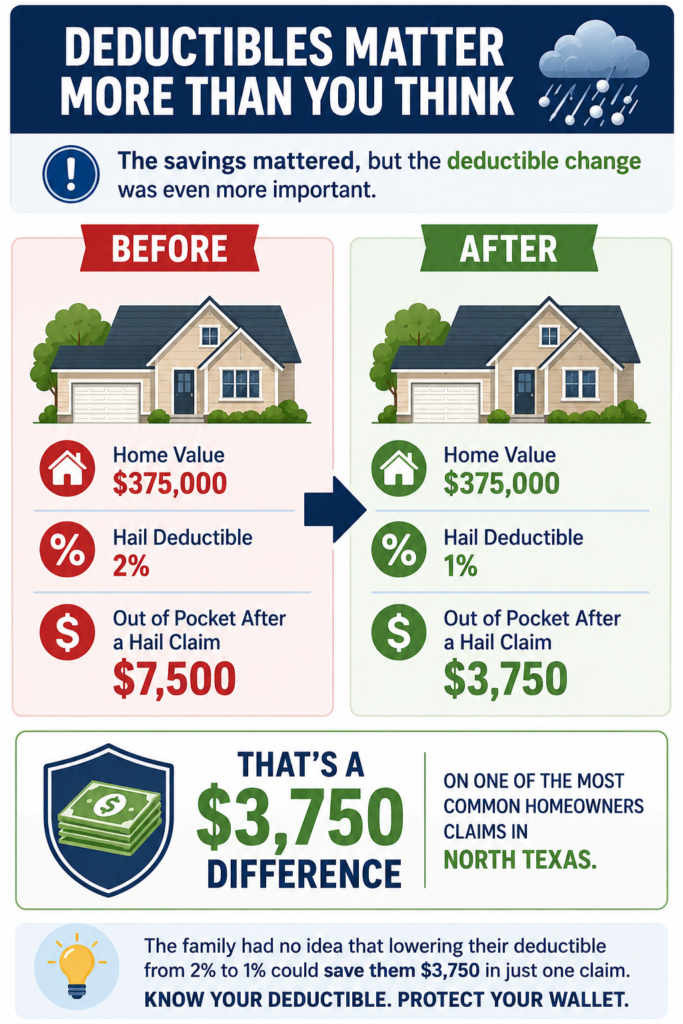

On a $375,000 home, that 2% deductible meant the family would owe $7,500 out of pocket after a hail claim.

Their auto policy was with a separate direct carrier online.

The auto coverage itself was adequate, but because the policies were split between companies, no bundle discount had ever been applied.

The issue was not that either policy was bad. The issue was that nobody had reviewed them together as a complete insurance strategy.

What Changed After Bundling

After comparing multiple carriers, we moved both policies to Travelers.

New Homeowners Policy

- New premium: $3,140/year

- Savings: $640/year

- Wind and hail deductible reduced to 1%

- Sewer backup coverage added

- Service line coverage added

- Dwelling coverage updated to current rebuild costs

New Auto Policy

- New premium: $1,850/year

- Savings: $360/year

Total Savings

- Previous combined premium: $5,990/year

- New combined premium: $4,990/year

- Total annual savings: $1,000/year

That works out to roughly $83 per month.

The Bigger Win Was the Deductible

Like many homeowners, they focused on premium price without fully understanding how the policy would actually respond after a major loss.

Frequently Asked Questions

Does bundling home and auto insurance always save money in Texas?

Not always, but in the vast majority of cases, yes. Most major Texas insurance carriers offer a multi-policy discount ranging from 15% to 25% off your total premiums when you bundle your homeowners and auto insurance under one roof.

Can bundling insurance actually improve my coverage limits?

Yes. When an independent broker reviews both policies together, they don’t just look for discounts—they fix structural flaws. As seen in this case study, bundling allowed the family to update their outdated dwelling values and unlock a lower wind/hail deductible that they couldn’t get with split policies.

Why was the deductible so important in this case?

Reducing the hail deductible from 2% to 1% lowered the family’s out-of-pocket exposure by $3,750.

Is it better to use an independent broker or a direct company to bundle?

An independent insurance broker is generally better because they are not loyal to just one company. A direct captive agent can only sell you their single bundle rate, while an independent broker can shop your home and auto package across 40+ competing carriers at once to find the absolute deepest bundle discount.

How often should North Texas homeowners review their bundled policies?

You should have your insurance policies reviewed at least once a year, typically 30 to 45 days before your annual renewal dates. Texas rates fluctuate frequently due to storm patterns, and an annual review ensures your premium stays competitive.

The Real Value of Reviewing Your Insurance Together

This Roanoke family originally wanted to know whether they were paying too much for insurance. What they discovered was that the bigger issue was not just premium cost, it was coverage structure and deductible exposure.

By bundling their homeowners and auto insurance through an independent broker, they saved $1,000 per year, improved their coverage, and reduced their potential out-of-pocket costs after a hail claim.

At Neill Insurance Brokers, we help North Texas homeowners review their policies together so they can better understand pricing, coverage gaps, and long-term protection strategies. Because sometimes the biggest insurance savings come from fixing problems you did not even know existed.