By Scott Neill | Published: March 18, 2026 | Last Updated: June 2026

Quick Summary

This article explains the differences between general liability and professional liability insurance for Texas businesses, detailing what each policy covers and which types of businesses typically need them. It highlights common scenarios where having the wrong coverage can lead to denied claims, helping business owners in Texas choose the right insurance to avoid costly gaps.

Key Takeaways:

- General liability insurance covers third-party claims involving bodily injury, property damage, and advertising injury during normal business operations.

- Professional liability insurance protects against claims arising from mistakes or errors in professional services, such as incorrect advice or design flaws.

- Texas businesses that perform physical work or interact with clients on-site often need general liability insurance, while those providing professional services typically require professional liability insurance.

- Having only one type of insurance when both are needed can result in denied claims and financial risk, so understanding your business activities is key to selecting appropriate coverage.

In 2026, Neill Insurance Brokers notes that Texas businesses generally need General Liability for physical accidents and Professional Liability for errors in advice or design. Most contractors and consultants require both to protect against property damage and financial loss claims, ensuring full compliance with state licensing and client contract requirements.

What General Liability Insurance Covers

General liability insurance, often called GL, protects businesses from third-party claims involving physical damage or injuries. These claims typically happen during normal business operations.

A standard general liability policy generally covers three main categories.

Bodily Injury

Bodily injury claims happen when someone is injured because of your business operations.

For example, imagine a client visiting your job site trips over equipment and breaks their wrist. General liability insurance may cover the injured person’s medical bills, legal expenses, and potential settlement costs.

Property Damage

Property damage coverage applies when your business accidentally damages someone else’s property.

For instance, if a plumbing contractor accidentally damages a client’s flooring while installing a water heater, general liability insurance may cover the cost of repairs.

Advertising Injury

Advertising injury claims involve issues such as copyright infringement, trademark disputes, or accusations of misleading advertising.

If a competitor claims your marketing materials copied their branding or messaging, general liability insurance may help pay legal defense costs.

What General Liability Does Not Cover

General liability policies have important limitations.

GL typically does not cover:

- Mistakes in professional advice or design

- Contract disputes

- Employee injuries, which are covered by workers compensation

- Damage to your own business property

What Professional Liability Insurance Covers

Professional liability insurance, often called Errors and Omissions insurance or E&O, protects businesses against claims related to mistakes in professional services.

Instead of covering physical accidents, this policy focuses on financial harm caused by professional errors, negligence, or failure to deliver services as promised.

Professional Errors

If a professional mistake causes a financial loss for a client, E&O insurance can help cover legal costs and potential damages.

For example, an architect’s design mistake might lead to structural problems in a building. Professional liability insurance can help cover legal defense and the cost of resolving the claim.

Negligence or Bad Advice

Many businesses provide advice or recommendations that clients rely on.

If a financial advisor recommends an investment strategy that leads to major losses and the client claims the advice was negligent, professional liability insurance may help defend the claim.

Failure to Deliver Services

Professional liability insurance can also apply when a business fails to deliver services as promised.

For example, if an IT consultant installs software that fails and causes a client to lose revenue, the client may pursue legal action for damages.

What Professional Liability Does Not Cover

Professional liability insurance also has exclusions.

It generally does not cover:

- Physical injuries to people

- Property damage

- Employee related claims

- Intentional wrongdoing or fraud

This is why many businesses need both general liability and professional liability coverage.

Which Texas Businesses Typically Need Each Type?

The type of coverage your business needs usually depends on whether your risks are physical, professional, or both.

Businesses That Usually Need General Liability

Many trade and construction businesses primarily face physical risks. These businesses typically need general liability insurance.

Examples include:

- Plumbers

- Electricians

- HVAC contractors

- Roofers

- Landscapers

- Painters

- General contractors

In these industries, the most common claims involve property damage or bodily injury on job sites.

If your business mainly performs physical work and does not provide professional consulting or design services, general liability coverage may be the primary policy you need.

Businesses That Usually Need Professional Liability

Some businesses provide specialized advice or services rather than physical labor. These businesses often need professional liability insurance.

Examples include:

- Consultants

- Accountants

- Insurance agents

- Financial advisors

- IT professionals

- Real estate professionals

The primary risk in these industries is that a client claims the advice or services caused financial harm.

Many of these businesses still carry general liability coverage for office risks, but professional liability is usually the more critical protection.

Businesses That May Need Both

Some industries face both physical and professional risks.

These businesses often benefit from carrying both general liability and professional liability coverage.

Examples include:

- Design build contractors

- Architects and engineers

- Marketing agencies

- Property managers

- Medical professionals

- Construction consultants

These businesses may create designs, provide professional advice, and perform physical work, which creates multiple types of liability exposure.

Frequently Asked Questions

Is general liability insurance required in Texas?

Texas law does not require most businesses to carry general liability insurance. However, many clients, landlords, and contracts require it before you can begin work.

Do contractors in Texas need professional liability insurance?

Most trade contractors only carry general liability insurance. However, contractors who provide design services, consulting, or project management may also need professional liability coverage.

Can a business have both policies?

Yes. Many businesses carry both general liability and professional liability insurance because they protect against different types of claims.

What is the difference between E&O and general liability?

General liability covers physical risks such as bodily injury and property damage. Errors and Omissions insurance covers financial losses caused by professional mistakes or negligence.

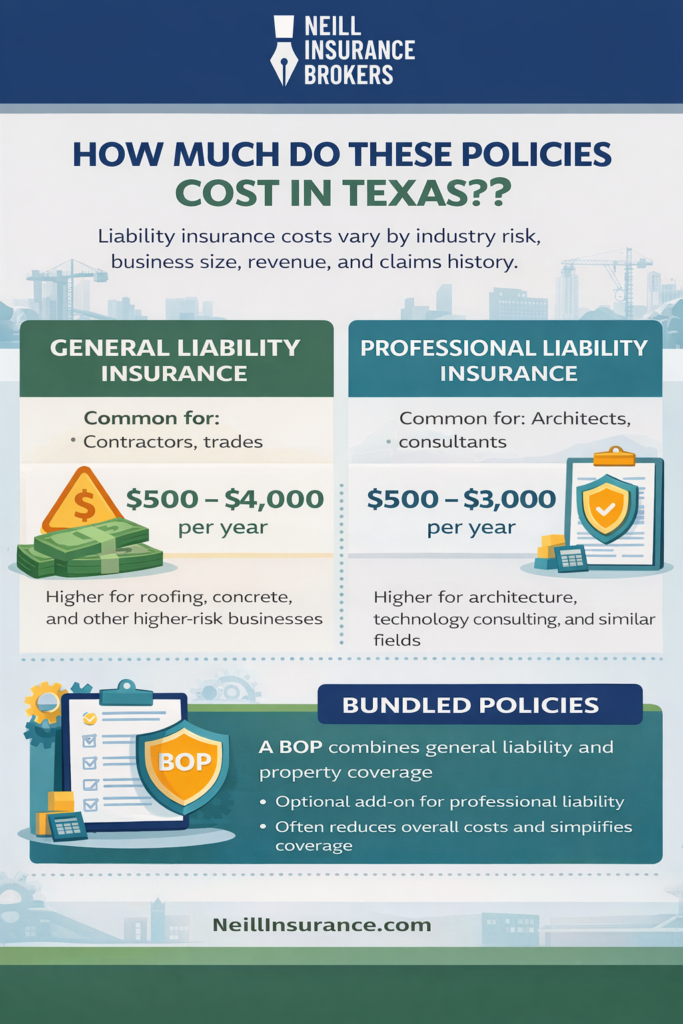

Does a Business Owner’s Policy include professional liability?

Most Business Owner’s Policies include general liability and property coverage. Professional liability is usually purchased separately or added as an endorsement depending on the insurer.

Protecting Your Business with the Right Liability Coverage

Understanding the difference between general liability and professional liability insurance can help you protect your business from costly claims.

General liability protects against accidents that cause physical injuries or property damage. Professional liability protects against claims involving mistakes in professional services.

Depending on the type of work your company performs, you may need one policy or both.

Neill Insurance Brokers works with business owners across Roanoke and throughout Texas to help them choose coverage that fits their operations and budget. If you would like help reviewing your options, request a custom quote to get started.