By Scott Neill | Published: April 8, 2026 | Last Updated: July 2026

Quick Summary

In partnership with Neill Insurance Brokers, this article explains the five essential homeowners insurance endorsements that most Texas homeowners lack, detailing what each covers, their typical costs, and the financial risks of not having them. It also guides readers on how to review their policies to ensure they have adequate protection against common Texas-specific risks like water damage, sewer backups, and roof replacement costs.

Key Takeaways:

- Water Damage Coverage protects against sudden internal water damage from burst pipes or appliance failures and typically costs $50 to $150 per year, potentially saving you $8,000 to $25,000 in repairs.

- Sewer and Drain Backup Coverage covers damage from backed-up drains or sump pump failures, costing $40 to $100 annually, and helps avoid costly mold-related expenses that can exceed $10,000.

- Service Line Coverage insures underground utility lines prone to damage from soil shifts in North Texas, costing $30 to $60 per year and covering repair claims between $3,000 and $10,000.

- Roof Replacement Cost Coverage ensures full replacement cost for your roof rather than a depreciated payout, typically costing $100 to $300 more annually and preventing significant out-of-pocket expenses on older roofs.

In 2026, essential Texas endorsements include Water Backup for sewer failures, Foundation/Water Seepage to cover slab issues, and Replacement Cost on Contents to avoid depreciated payouts. Having spent 10 years as a captive Farmers agent before founding Neill Insurance Brokers, Scott Neill has reviewed hundreds of North Texas residential policies. Managing 304 active homeowner policies right here in our community, he stresses that adding Mold Remediation and Equipment Breakdown coverage is also critical to closing gaps standard policies exclude, protecting you from Texas’s unique environmental and mechanical risks.

Why Home Insurance Coverage Has Changed in Texas

Home insurance policies used to cover more by default.

Today, many important protections are optional, and most homeowners do not realize what they are missing.

Insurance carriers have tightened coverage over the past decade, especially in North Texas where hail, water damage, and foundation issues are common.

What used to be included is now an add on. And if it is not added, it is not covered.

If your policy was written a few years ago, or set up quickly during closing, there is a strong chance you are missing key protections.

The 5 Endorsements Most Texas Homeowners Are Missing

These endorsements directly impact whether a claim is covered or denied.

1. Water Damage Coverage

What it covers:

Sudden and accidental water damage inside your home, such as burst pipes, appliance failures, and overflow events.

Typical cost:

$50 to $150 per year

Potential out of pocket cost without it:

$8,000 to $25,000

2. Sewer and Drain Backup Coverage

What it covers:

Water entering your home from backed up drains, sump pump failures, or municipal sewer issues.

Typical cost:

$40 to $100 per year

Potential out of pocket cost without it:

$10,000 to $30,000

In Texas heat, mold can begin forming within 24 to 48 hours after a backup event, increasing the total cost quickly.

3. Service Line Coverage

What it covers:

Underground utility lines connecting your home to the street, including water, sewer, and electrical lines.

Typical cost:

$30 to $60 per year

Typical claim range:

$3,000 to $10,000

North Texas soil shifts frequently, which puts stress on underground lines and increases the likelihood of failure.

4. Roof Replacement Cost Coverage

What it covers:

Full replacement cost for your roof instead of depreciated value.

Typical cost difference:

$100 to $300 per year

Why it matters:

Actual cash value policies reduce your payout based on age.

Example:

A $15,000 roof with 40 percent depreciation pays $9,000. You cover the remaining $6,000, plus your deductible.

5. Scheduled Personal Property

What it covers:

High value items like jewelry, watches, art, and cameras at their full appraised value.

Typical cost:

1 to 2 percent of the item’s value annually

Why standard coverage falls short:

Most policies limit jewelry coverage to $1,500 to $2,500 per claim.

A Common Misconception That Costs Homeowners Thousands

Many homeowners believe their policy covers everything inside and around their home.

In reality, coverage is only as strong as the endorsements included.

Lower premiums often mean fewer protections. That is not always a bad decision, but it should be intentional.

Insurance is not just about price, it is about what happens when something goes wrong.

Frequently Asked Questions

What is an endorsement in homeowners insurance?

An endorsement is an add on that modifies your base policy to include additional coverage or protection.

Are endorsements required?

No, but many are essential for proper protection, especially in Texas where certain risks are more common.

Why are these coverages not included automatically?

Insurance carriers separate these coverages to control risk and keep base policy premiums lower.

How much do endorsements typically cost?

Most endorsements cost between $30 and $300 per year depending on the type of coverage.

How do I know which endorsements I need?

It depends on your home, your risk exposure, and your financial situation. A policy review can help identify gaps.

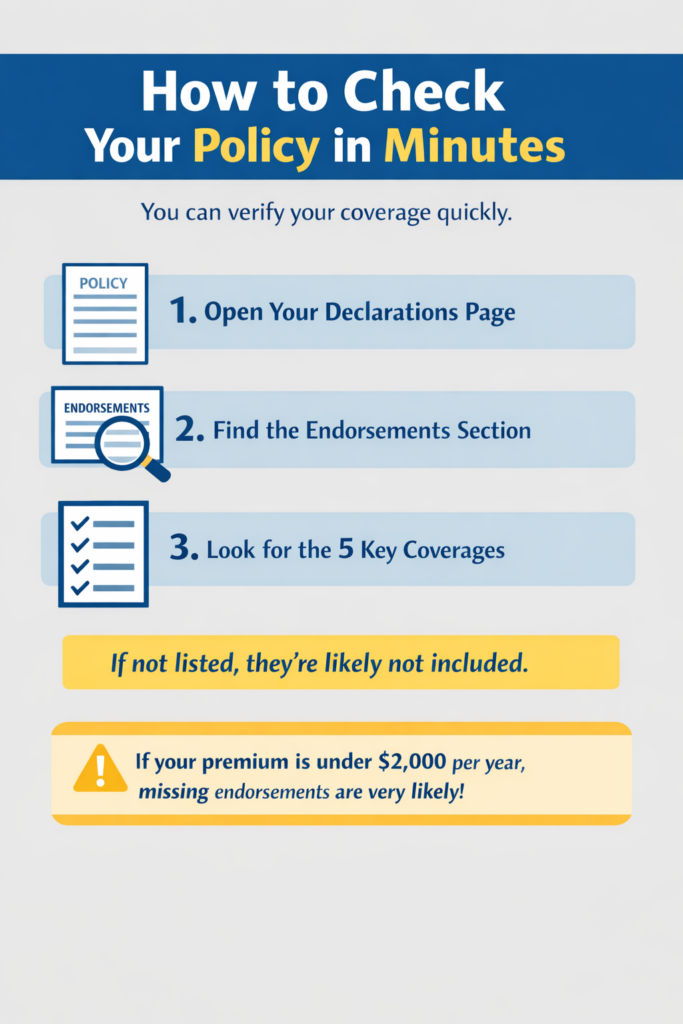

Know What Your Policy Actually Covers

If you have not reviewed your homeowners insurance recently, there is a good chance you are missing important coverage. Most homeowners do not find out until they file a claim, and by then it is too late.

Now you know the five most commonly missing endorsements, what they cost, and how they impact real world claims. The next step is simple. Make sure your coverage matches your risk.

At Neill Insurance Brokers, we help Texas homeowners review their policies, identify missing protections, and build coverage that actually works when it matters.

Request a policy review and see exactly where you stand.